Space Education News

Space Industry Growth: Where Are the Opportunities in 2022?

Written by: Space Foundation Editorial Team

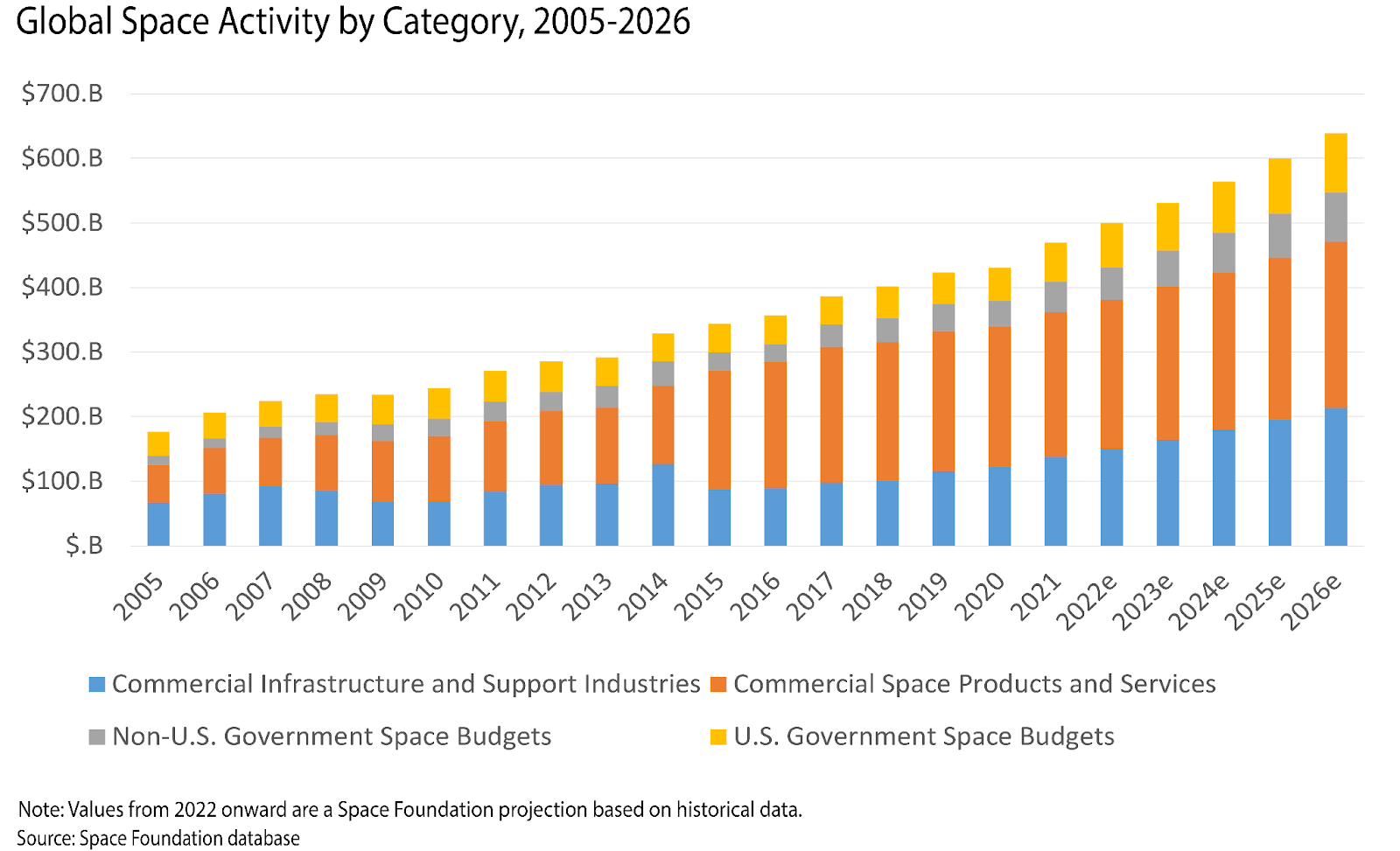

The global space economy hit $469B in 2021, growing at the fastest annual rate in seven years. In the first six months of 2022 alone, a record-setting 1,022 spacecraft were placed in orbit—more than in the first 52 years of the Space Age (1957-2009, 986) combined.

Space industry opportunities abound, but the global space ecosystem is vast. Where are the areas of greatest space industry growth in 2022?

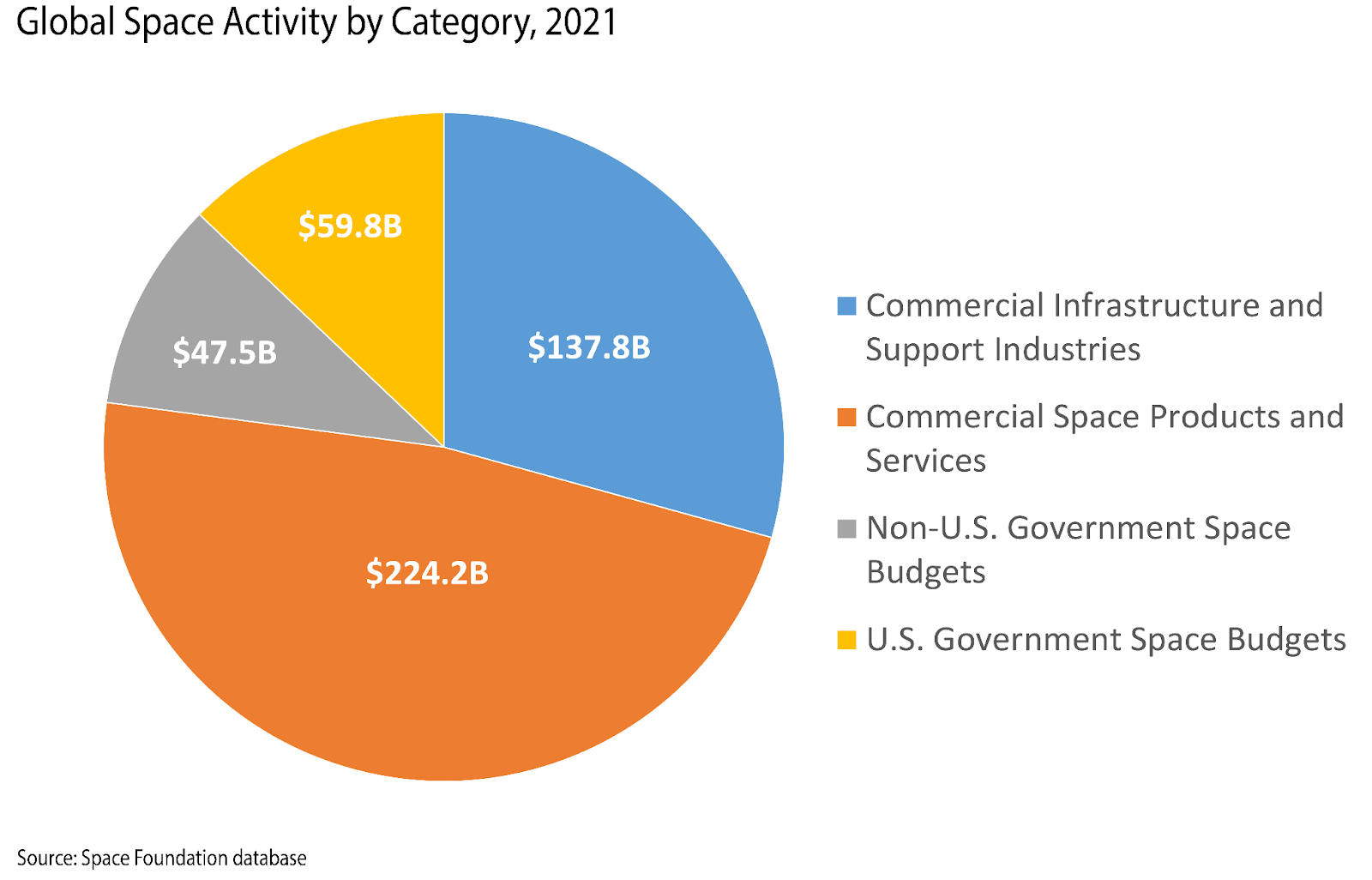

Global Space Industry Growth by Category and Sector

Government vs. Commercial

According to The Space Report, government space budgets worldwide reached $107.3B in 2021—an increase of 19% over the previous year. Over 90 countries now operate in space. Of those, eight (the U.S., China, Russia, the European Space Agency, India, Iran, Israel and Japan) launch consistently and can obtain orbital access.

The U.S. remains far and away the biggest space spender, with a $59.8B annual budget that is more than all other countries combined. The U.S. increased its space budget by 18% in 2021, while the next largest, China, increased by 23%. India and multiple European countries increased space spending by 30% or more.

However, while $107B in government space spending is significant, it makes up less than a quarter of total global space activity.

Commercial space leads the way, reaching $362B in global space activity in 2021. Over 90% of today’s spacecraft are commercial, with 14 companies that regularly launch, have recently reached orbital space, or have acquired companies with orbital launch capability. Ten additional companies are close to a launch debut.

Commercial Infrastructure vs. Space Products & Services

For many, “commercial space” brings to mind human spaceflight. This is a crucial part of the commercial space industry and generates the most headlines, but it is not the largest or fastest growth area.

Commercial Infrastructure and Support Industries—which includes human spaceflight, on-orbit satellite servicing, and ground stations and equipment—made up $137.8B of global space activity in 2021. By contrast, Commercial Space Products and Services reached $224.2B in the same year—nearly half of all global space activity, both government and commercial.

Examples of space-based products and services include broadband and GPS. A May 2022 report by Citigroup identified the satellite market as the most important driver of the overall space economy.

Space Industry Investment Activity

After breaking records in 2021, private investment in space companies has slowed in the wake of broader market concerns, inflation and supply chain issues. Space infrastructure companies brought in $2.5B in private investment in Q2 2022 (including $1.7B to SpaceX), representing a 45% drop from the same period in 2021.

M&A activity, too, has slowed. As per a Quilty Analytics report, there were six announced acquisitions and buyouts in Q1 2022 compared to 13 in Q1 2021 and 15 in the prior quarter.

However, industry experts such as Space Foundation’s CEO, Tom Zelibor, emphasize that the overall space economy is vibrant and growing, with strong government and commercial spending. In a Q1 2022 report, Justin Cadman and Chris Quilty of Quilty Analytics note that there are still healthy levels of M&A evaluation activity and that buyer interest remains high. The downshift may be a return to a more sustainable level of dealmaking activity after an “overheated” 2021.

Space Industry Growth Forecast

In their May 2022 report, CitiGroup analysts predict the space industry to reach $1T in annual revenue by 2040. This is in line with earlier forecasts by Space Foundation, Morgan Stanley and Bank of America. Reaching this benchmark, says Citi, is contingent on launch costs continuing to drop as they have in recent years. This will unlock the potential for more services from orbit, including consumer broadband, IoT networks and satellite imagery.

According to The Space Report, satellite-enabled key growth areas could include telecommunications, supply chain management, remote sensing (environment, agriculture, natural resources monitoring, weather), national security, and cybersecurity/encrypted applications in banking and finance.

Citi also predicts the fastest growth rate will come from new space applications and industries, with revenues rising from zero to $101B by 2040. “Space-as-a-service” applications could reach $17B in annual sales in 2040, according to Citi forecasts.

“Companies and individuals looking to make their mark on the global space economy should consider how each market serves their interests and how they can create direct terrestrial impact as their capabilities scale,” says space economy strategist Kelli Kedis Ogborn, Vice President of Space Commerce and Entrepreneurship at Space Foundation. “We need to envision the ways that space can serve us and recognize that we have the capacity to build out those ways and deliver on that promise.”

Space Commerce Institute can help you grow into and within the global space ecosystem.

Space Commerce Institute at Space Foundation connects you to the dynamic and growing space economy through education, experience, training, mentorship and consultancy. From online workshops to ad-hoc and project-based space industry consulting, Space Commerce Institute provides actionable and tangible programming that facilitates growth into and within the growing space industry. Explore Space Commerce Institute programming here.